I hope you found last month’s article beneficial, where I went through the changes made over the last few years and the difference of allowing directors to pay into their PRSA pensions without BIK. Email us if you do not have a copy.

This month we look at the change as a way of allowing directors and business owners to invest once again in property-based pensions. Due to European Company Law, it has been very difficult for several years for directors to directly purchase property and place it into their pension. However, PRSAs are a personal product and the same EU company laws don’t apply.

I will give two examples showing the difference between putting an active income (rent) into a tax-free

environment, and having funds in a normal fund-based PRSA. These are based on a large payment from your company into your pension for eight years, but this does not mean that you need to start your pension at these levels, rather they are there to show how a fully funded pension would work.

Let’s use Joe as a test case. Joe turned 40 in January and is going to pay €10,000 per month into his pension for eight years. We generally like to build a fund of €1 million before purchasing property,

therefore both examples are the same for the first eight years, ie €120,000 paid in per year

for eight years. To keep this comparison simple, we have used growth rates for the fund based PRSA as 4% per year with a total fund management charge of 1% per year. This applies to both examples for the first eight years. We also take an income in retirement of €100,000 increased by 2% per year from

both examples.

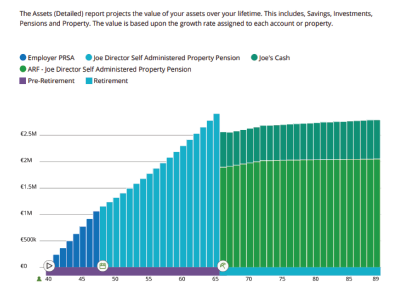

In Example 1, the dark blue graph shows the payments made into the fund for the eight years.

The light blue graph is as follows:

- Property values increase 2% per year

- Rental yield Gross 6% (We take 80% of the rent to be the net rent going into the pension, allowing for property management, insurances and maintenance.)

- Rental growth is projected at 2% per year. Dark green is your 25% of the fund taken at retirement – value €660,000 (Tax Efficient Cash) Light green is your fund after retirement, taking income of

€100,000 per year increasing at 2% per year.

As the illustration shows, the rent is effectively continuing to pay into the pension even though you are no longer paying in directly. As the property value and rent grows over time the fund continues to

grow. When you take your 25% (Approx €660,000) and then €100,000 per year you can see that the income you are taking is being replaced by the rent still coming into the fund. If you pass away as a 90-year-old you will leave approximately €2 million in your fund. When you die, the properties are sold

by the fund and the money distributed to your estate, to your spouse within the fund and later to your children, at a flat tax of 30% but with no inheritance tax. If you pass away before retirement the entire

amount is paid tax free to your spouse.

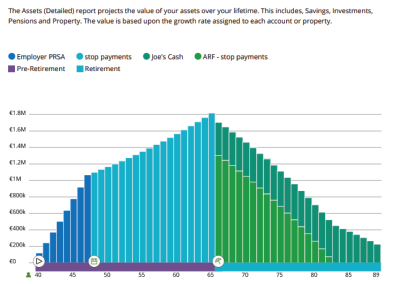

In Example 2 we apply the same returns as we did to the other fund, with the main exception being that

there is no rent. We continue to apply the 4% growth rate throughout the life of the fund. Again, as above, we pay into this fund for eight years at €120,000 per year and we then stop paying into the

fund. We also take €100,000 per year as income in retirement, increased by 2% a year.

- Dark blue signifies the steep growth where the pension is being paid into.

- Light blues hows growth at 4% per year on the value in the fund.

- Dark green represents 25% from the fund at retirement value of €403,000 (Tax Efficient Cash)

- Light green is your fund after retirement, taking €100,000 per year increasing at 2% per year.

As the graph shows, your pension will run out of funds in your mid-eighties. It is very important to note that this is just an example; it is not a forecast. We have used a few assumptions in making these graphs. Growth in the fund-based PRSA is at 4% per year, but this may be less as the value of funds can fall as well as rise.

In both funds you have paid in the same amount, so the difference is the active income. Rental income is difficult to manage personally (tax at up to 52%) or in a company as you have layers of tax. However, in the pension you have zero tax on the gain in property value, zero tax on the rent and zero tax to put the funds into the pension in the first place.

This article shows how a property-based pension might work, but like all things this is a risk investment. Property in ten years time might not be the investment it seems to be today and may very well be worth less. We assume that the Pension owner stays invested in property for the full term, but this is a high-risk product as the value of property and/or rent can go down as well as up. In the event that a director decides that they want to exit property in their PRSA, there is nothing to stop them from instructing the broker/trustee to put the properties up for sale.

Arm’s length rules apply here. You can’t sell to a connected party and you must use an auctioneer to sell the property on the open market. This is a self-administered product and you are taking the risk that any property you decide to purchase is a good and viable property.

Our recommendation is that a scheme should own 100% of a property, and not a share, or part, of an investment property. A small multi-unit building in a good rental area is usually a viable target for your pension fund.

When you take the fact that you paid no tax on the money you put in to the scheme to get it up and running, and no tax on the rent or the capital gain, it is one of the most effective compounding investments available.

At MoneyTree we have the right agencies and authorisations to help directors take advantage of this pension opportunity, so why not give us a call. We can see where your existing pension planning is now, and if we can combine that with more funding to position you to take advantage of this over the next several years.

Or, if you have no pension planning at all, we can help you to set up and get you started in a normal PRSA fund. This is a great starting point for any director to create their own pension experience.

Warning: These figures are estimates only. They are not a reliable guide to the future performance of your investment.

Warning: The value of your investment may go down as well as up. You may get back less than you invest